Semiconductor Sovereignty

New chip tariffs can promote domestic manufacturing and secure America’s future.

By Jason Hausenloy, independent AI policy researcher and writer

Last week, the Department of Commerce launched an investigation to introduce tariffs on semiconductor imports, with an eye for developing the potential for U.S. domestic production of computer chips. President Trump announced there would be new tariff rates on imported semiconductors “within the coming week.” Such a move would serve as a vital boost to domestic manufacturers of computer chips: the technological source of modern life.

Such tariffs present a singular opportunity to reshore high-end manufacturing. Additionally, this would reduce American reliance on Taiwan, which produces over 60% of semiconductors and, of the cutting-edge frontier chips, manufactures over 90%. Such reliance on an earthquake-prone island that China considers fully its own leaves U.S. national security and economic competitiveness to the whims of the Chinese Communist Party.

Designing these intelligently can minimize the short-term costs for American AI companies today while building long-term strategic capacity. While American companies will face temporary price increases (not exceeding the tariff percentage), the resulting domestic semiconductor capacity delivers security benefits that decisively outweigh these costs.

America’s Semiconductor Decline

It may seem odd that the United States, long the first mover in computer technology, has to worry about the global semiconductor supply. The U.S. lost its semiconductor manufacturing dominance through a series of strategic missteps beginning in the 1980s. American companies like IBM and Intel pioneered integrated circuit technology (the core of a computer chip), but they prioritized spending time on design over fabrication, outsourcing manufacturing to lower-cost Asian foundries while focusing on higher-margin chip design. This trend accelerated in the 1990s as Taiwan and South Korea offered massive government subsidies, tax breaks, and built specialized industrial clusters while U.S. policy remained hands-off.

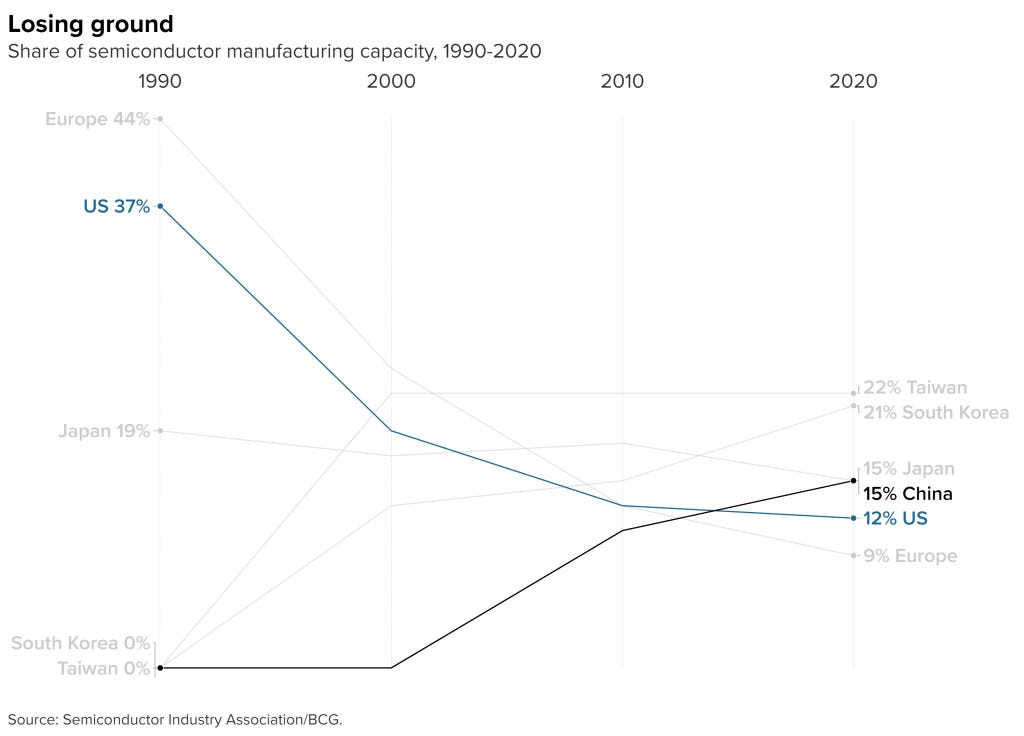

When manufacturing costs for leading-edge chips skyrocketed (exceeding $10 billion per factory by the 2010s), American firms increasingly adopted the ‘fabless’ model, with companies like Nvidia, AMD, and Apple designing chips that relied on cheaper labor overseas to manufacture. Meanwhile, the Taiwanese Semiconductor Manufacturing Company (TSMC) invested relentlessly in manufacturing technology, outspending American competitor firms while attracting top engineering talent from American universities. By 2020, U.S. domestic manufacturing capacity had plummeted from 37% of global supply in 1990 to merely 12%, with not a single company capable of producing the most advanced chips on American soil. As everything from cars to cookware has become increasingly reliant on the latest and greatest semiconductor technology, a lack of access—or the threat thereof—presents a risk to the fundamentals of modern life.

And while that outsourcing has gone to a U.S. ally, its geography is perilous. The concentration of advanced chip production in Taiwan creates significant supply chain vulnerabilities for the United States. China could weaponize this concentration—either through pressure on Taiwan or in a military confrontation. Furthermore, U.S. dependence on Taiwan, which China considers a province, heightens tensions by pushing the United States to defend its chip supplier.

A Domestic Chip Revival?

Combatting the decline in domestic production, the Trump administration has succeeded in beginning to bring semiconductor manufacturing back home. Across the chip supply chain, from Micron to Apple to Samsung, companies have committed to hundreds of billions of dollars of expansion. Most significantly, Nvidia recently announced it would begin manufacturing its Blackwell series (one of its cutting-edge chips) at TSMC’s Arizona plant. However, TSMC’s effort to move production to the United States has been slow. Their plant in Arizona has been plagued by delays arising from stringent permitting and environmental regulation, and it does not produce the latest chips, despite receiving over $6 billion in subsidies from the CHIPS and Science Act.

The CHIPS Act represents the most significant government effort to address America’s semiconductor decline, having already catalyzed over $300 billion in private investment in domestic chip manufacturing. But while the CHIPS Act has helped spur the industry, it has also introduced burdensome regulatory requirements that companies only follow because they want the associated subsidies. It requires applicants to provide “equity strategies” promoting diversity and inclusion, develop “Supplier Diversity Plans” for minority-owned businesses, and submit detailed “Climate and Environmental Responsibility Plans”—none of which directly support increased semiconductor production. Beyond those specific rules, TSMC’s Arizona plant has struggled with America’s labyrinthine permitting process, ambiguous environmental regulations, and a shortage of specialized semiconductor engineers—systemic barriers that would hamper domestic chip production regardless of whether companies are motivated by subsidies or tariffs. These Biden-era rules, which are not statutorily required, should be waived, and the broader bureaucracy should be reformed.

In the short-term, a tariff-based approach would drive manufacturing relocation without these regulatory strings attached, and could help create incentives to overcome those systemic barriers. While this may cause temporary price increases, it creates resilience against supply disruptions that could occur when Taiwan’s chip production is threatened—a far more costly scenario for the American economy.

These tariffs would directly incentivize Taiwanese firms to build manufacturing in the United States by making exporting more expensive and, if designed well, offer tariff reductions if investment in the United States increases. Furthermore, this approach works through existing customs systems without requiring new government offices or complex application processes. Tariffs can be implemented quickly and adjusted as needed, avoiding the delays and political complications that have hindered CHIPS Act implementation thus far.

New tariffs on Taiwanese semiconductors are therefore vital for American national security. The alternative is that adversaries, like China, can unilaterally decide to cut off chip production to its whims, and they may do so when they believe cutting chips to U.S. firms would cause the most damage.

Tariffs, if implemented well, can give the United States sovereignty over its own future. One initial approach may be to target investment in manufacturing directly and make the tariff proportional to the fraction of total investment that does not go to the US.

What Implementation Could Look Like

But what could the Trump administration’s semiconductor tariffs look like? To provide maximum encouragement, Taiwanese chip companies that keep their investments exclusively in Taiwan or other non-U.S. locations should face a full 100% tariff on imports (as President Trump spoke about on the campaign trail). The carrot would come when they start to move.

As firms shift investment to American soil, Taiwan’s tariff rate could drop proportionally based on the ratio between their foreign and domestic investments, with the goal of moving as much production stateside as possible. Taiwan, to its credit, has already promised a $100 billion investment commitment to the United States—new tariffs could help provide stronger incentives for the island to fulfill, and hopefully exceed, that figure.

Using current figures—$11 billion in announced U.S. investment through 2030 compared to all non-US investment of $21 billion—the above proportional rate would produce an initial 66% tariff on semiconductor chips from Taiwan. This scheme should be applied globally, but, given Taiwan makes 90% of advanced AI chips, will, in practice, end up affecting Taiwan most.

Unlike the CHIPS Act’s complex grant-making process requiring extensive bureaucratic oversight of DEI mandates and climate plans, this mechanism operates through existing customs infrastructure with simple metrics. That’s because companies self-report verifiable investment data quarterly, leaving Commerce Department officials to calculate the ratio, and then customs officials could apply the resulting tariff percentage. This eliminates the need for a large grant-reviewing bureaucracy while delivering faster results.

However, we must acknowledge the practical realities of semiconductor manufacturing. Chip-making is a slow business. TSMC is already producing close to capacity. Therefore, any tariffs will only influence future investment and should be calibrated accordingly. TSMC could secure a 0% tariff rate on its production today if all of 2025’s investment was in the United States exclusively.

One worry may be that Taiwan maintains the most advanced manufacturing capacity as a ‘silicon shield’—whereby Taiwan’s semiconductor dominance compels the United States to defend it, while simultaneously deterring Chinese aggression due to Beijing’s reliance on these chips—while only peripheral facilities move overseas. A new American fab churning out iPhone chips, where only testing and packaging is done in the United States, helps little with manufacturing capacity or national security when the true strategic assets remain offshore. Countries that can manufacture the most advanced semiconductors will gain decisive advantages in AI deployment and development that will determine economic and military supremacy.

Therefore, it could be worth tracking what percentage of semiconductor value is actually created on American soil through domestic manufacturing processes. To capture this in the tariff, officials could calculate the total value-added in the United States, and then weigh the tariff by that amount. Value-added is calculated as the difference between input costs and final product value—if a $20,000 chip requires $10,000 in materials, with $5,000 in fabrication and $5,000 in testing, moving only testing to America would represent just 25% value-added domestically. The goal of reshoring domestic semiconductor manufacturing is to return full-lifecycle supply chains to America, not just some of the components.

Finally, these could be paired with complementary policies, including waiving Biden-era implementation requirements for the CHIPS Act (which are not statutorily required), revitalizing America’s export industries, and liberalizing immigration for top scientists.

What it All Means

The world’s most valuable technology is manufactured almost exclusively in one of its most volatile regions. The frontier chips at stake will power the training and deployment of AI systems—the technology that will define military supremacy and economic competitiveness for decades. And after decades of determined effort, liberal poaching, and massive state investment, China has narrowed the semiconductor manufacturing gap significantly, with companies like SMIC now producing 7nm chips.

Domestic production of the chips that power modern life is vital to America’s future. In a speech last week, Michael Kratsios, the director of the Office of Science and Technology Policy, highlighted the need to “establish secure supply chains” and “create investment incentives to reshore manufacturing.”

Without decisive action to secure domestic production of advanced semiconductors, America risks ceding the foundation of its technological advantage to foreign powers who don’t share our values or interests. As the President warned, “rivals abroad seek to usurp America’s position as the world’s greatest maker of marvels.” Don’t let them succeed.